Your pet is part of your family. If something happens to your furry friend, it can cause a significant amount of stress.

Whether it's an unexpected accident or illness, you'll want to make sure your pet has the best care.

Unfortunately, the cost of vet bills can quickly add up. Paying for animal care can cause a strain on your budget, and sometimes hard choices need to be made.

Pet insurance can help protect your finances and reimburse you for some of your out-of-pocket vet expenses. But how does it work? And is there a catch?

Read on because we're about to tell you how pet insurance works.

Pet insurance has been available in the US since the '80s. Today, there are around 25 insurance agencies that offer this service.

Most pet insurance companies provide coverage for cats and dogs. Some insurers also offer plans for other animals, such as rabbits, horses, and exotic pets. If you sign up for a policy, you can expect to be covered in both the US and Canada.

Pet insurance comes with premiums, deductibles, and annual limits. There are also inclusions and exclusions. If you do visit a veterinarian, you'll be reimbursed a percentage of the fees, depending on the policy you have.

How do pet insurance policies work? Before you sign up for a policy, we'll give you a rundown of what to expect.

Keep in mind that this service is like human health insurance and helps you pay for medical expenses, including veterinary bills. If you're looking for coverage against damage caused by your furry family member, consider animal liability insurance instead.

And if you rent, acquiring pet insurance and animal liability insurance can help you secure rental property by establishing you as a responsible pet owner.

PetScreening gives your pet a score based on a range of factors — not just the breed. Learn more.

Now, let's chat about pet insurance.

The first step is to choose a provider and a policy. For pet parents, comparing these platforms can be confusing, so think about what's important to you.

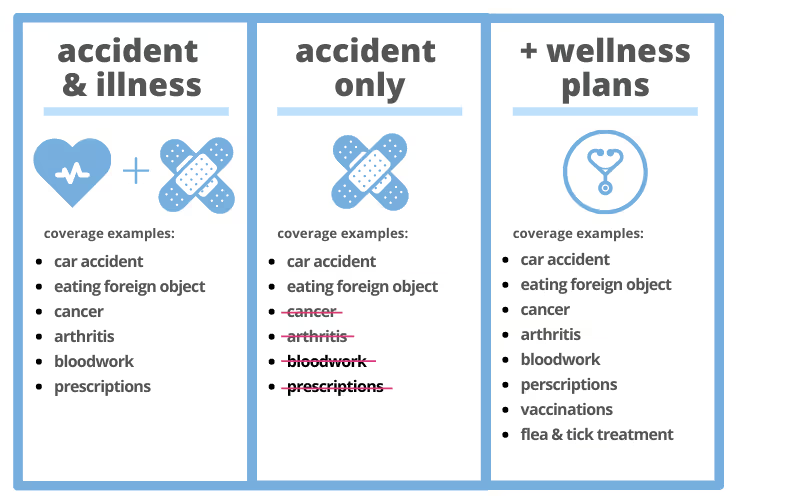

For example, most providers offer illness and accident coverage, accident-only plans, and optional pet wellness plans, like:

Illness and accident: the most comprehensive plan. Expect coverage for unexpected illnesses, broken bones, emergency clinics, chronic conditions, and more.

Accident only: for unexpected expenses due to an emergency. Think broken bones, cuts, and the ingestion of toxic substances.

Wellness: optional benefits, such as preventative procedures, alternative therapies, and annual wellness exams.

Each policy will come with a list of eligible conditions. If your pet already has health issues, these are called pre-existing conditions and aren't usually covered. There'll also be a list of exclusions, such as pregnancy and dental care.

Before you choose a provider, compare plans side by side and read reviews to learn how easy it is to make a claim.

Every month you’ll pay a premium. It’s usually affordable but will vary depending on your plan.

Besides the coverage options, you'll also choose how much the insurer will contribute toward your veterinary expenses — this can be up to 90%. And you'll need to choose a deductible, which is the amount you'll pay before the insurer's contribution.

Most companies will give you a pet insurance quote based on your unique circumstances. The type of animal, age, location, and health can all play a role in the final monthly premium and deductible.

Just because you've paid your first premium, it doesn't mean your pet will be covered straight away.

Your pet health coverage will usually come with a waiting period. Make sure you read the fine print because this can vary between providers and illness types. As an example, Pumpkin Insurance has a 14-day waiting period for all illnesses and accidents.

Once the waiting period is over, you can get your pet the treatment they need — without breaking the bank.

If your pet needs medical care, check to see if it's covered in your plan.

The good news is that most providers will let you choose your own veterinary care. For example, it could be a local vet, specialist, or an emergency animal hospital.

As long as the vet is licensed, you’ll be eligible for reimbursement.

So, your pet has had an eligible accident or illness, and you've taken them to get vet care. What happens next? Does the insurance company pay the veterinary care provider?

No. Unlike health insurance, you’ll need to pay for your pet's bill at the time of treatment.

You have to cover the full amount until your claim is approved. Make sure you get a copy of the medical records and an itemized receipt from your vet, as you'll need these to make a claim.

After you've paid the vet, you can put in a claim for reimbursement. Most pet insurance companies have a time limit. For example, MetLife Pet Insurance requires claims to be submitted within 90 days of the treatment. On the other hand, the ASPCA (American Society for the Prevention of Cruelty to Animals) gives you up to 270 days.

There can be different options for making a claim. Depending on the provider, you may be able to submit the details via an app, an online portal, email, mail, or fax.

Remember, you'll need a copy of your veterinary treatment plan and your pet's medical bills to go with your pet insurance claim. Be as thorough as possible and double-check to make sure the information is accurate.

Once your claim has been processed, the insurer will give you the money via your preferred payment method.

Direct deposit is usually the quickest, but check payments may also be available.

It can take up to 30 days to receive your reimbursement (or longer if there are missing details). Despite this, most companies try to pay their customers within 5 to 14 days.

If you have questions about your reimbursement timeline, you can speak to the insurer’s customer service team.

Pet insurance plans do vary. However, there are a few common inclusions that you can expect.

These health conditions need to occur after your coverage starts:

Remember, not all of these will be covered straight away, and you usually have to pay a deductible. There will also be an annual expense limit.

Read your pet health insurance policy carefully, so you know exactly what's covered.

Pet insurance policies can be confusing, and you shouldn't assume your pet will be covered for every vet bill.

There's a long list of common exclusions, and we'll get to them shortly. But it's important to note that not all plans are the same. Some companies offer different levels, as well as wellness plans.

If you do choose a wellness plan, items on the common exclusions list may be included for an additional monthly fee.

Now for the common exclusions:

Accident and illness coverage can give you peace of mind. But if your pet has a pre-existing condition, it’s usually not covered.

Let's say you have a dog who has chronic allergies.

If you take out a policy, you won’t be covered for any allergy treatments. In fact, almost every pre-existing condition will be excluded, from cancer to diabetes to hip problems.

Even if your pet hasn't been diagnosed but is showing symptoms, you may be ineligible for coverage.

For example, if your cat has unexpected weight loss and you sign up for a policy before visiting a veterinary clinic, the resulting illness will still be classed as a pre-existing condition.

What if your pet has an illness but then recovers?

Most pet insurers understand things can change. If your pet is cured and has no ongoing symptoms, the pre-existing condition status will be removed.

Here's an example. ASPCA Health Insurance expects your pet to be free from symptoms, with no treatment for at least 180 days. After this time, the condition can be covered. However, if your dog or cat has ever had knee or ligament issues, they'll always be excluded.

If you are considering signing up for this type of insurance, we recommend doing it as early as possible. As animals age, the number of health issues can increase, adding to the list of excluded, pre-existing conditions.

To get an accurate picture of your pet’s health, the insurance company may ask for a vet check before the policy starts.

Yes. Most policies have a waiting period, but it won't be the same for every health condition. Accident coverage usually kicks in first, followed by illness coverage.

Pet insurance companies all have different waiting times, but you can usually find this information on the insurer's website.

As an example, Embrace Pet Insurance offers a 48-hour waiting period for accidents. Illness plans are valid after a 14-day waiting period. If you have a dog, your pampered pooch will have to wait six months for the treatment of any orthopedic conditions.

Compare this to Spot Insurance, a company with a standard 14-day waiting period across its pet policies.

There is also a minimum age to enroll your pet. For kittens and puppies, it’s usually between six and eight weeks. Some companies also have a maximum age for new policies.

When comparing policies, make sure you look at the maximum payout limits. Each insurance agency has its own rules, and the plans can vary significantly.

Check for an annual limit. This is the maximum amount you'll be reimbursed for over a 12-month period. For example, you may be covered for up to $2,500, $5,000, or $10,000.

If your vet bills are over this amount, you'll pay the difference.

Additionally, any deductibles you've paid are not included in this total. So, if your deductible is $100 and the total bill is $1,000, $900 will go toward your yearly limit.

Some companies don't have an annual limit but may have a lifetime limit instead.

Individual conditions may also have their own specific limits. As an example, if your dog gets diabetes, there may be a maximum amount you can claim for the treatment of this illness.

This maximum payout limit can impact the cost of your monthly premium.

Most pet insurance companies cater to dogs and cats. But what if your pet doesn't “meow” or “woof”?

Some insurers, such as Nationwide Pet Insurance, will also cover other animals, such as birds, reptiles, and exotic pets.

Then, there are companies that specialize in animal insurance for horses, pigs, rabbits, and rodents.

If you have more than one pet with the same insurer, you'll usually get a multi-pet discount. The amount varies, but you can expect a discount of between 5% and 10%.

Pet ownership comes with lots of perks. Depending on the animal, you may get a friendly face whenever you walk in the door, a companion to walk with, or free affection whenever you need it.

However, caring for a pet isn't cheap. Besides food, entertainment, and training, there are veterinary costs. From emergency injuries to chronic illnesses, the cost of treatment can quickly add up.

To help you cover any future bills, you may be thinking about pet insurance. You'll pay a monthly premium, and if your pet does need medical treatment, some of the costs may be reimbursed.

The type of plan you choose will depend on a range of factors, including the age of your pet, any pre-existing conditions, and your location.

Want to rent with a pet?

Want to encourage your renters to be responsible pet owners if you run a pet-passionate property?

Check out PetScreening’s services. We simplify the process of running rental properties for landlords and getting a new property for renters by providing services, like digital passports for dogs and cats.

If you simply want to read more informative articles on pets, property management, and associated policies head to the Bark Library.